TL;DR:

- Trading with funds from prop firms eliminates personal capital risk, enabling traders to operate under structured risk controls. This approach provides access to larger capital, promotes disciplined trading behaviors, and allows profit sharing, all while safeguarding personal savings. Success depends on mastering risk management, consistency, and understanding evaluation rules within these no-risk models.

Most retail traders assume that serious trading requires serious personal savings on the line. That assumption is wrong, and it costs traders both money and opportunity. The benefits of no personal capital risk trading models are well documented: you access institutional-level buying power, operate under structured risk controls, and keep your personal finances intact regardless of trading outcomes. Prop trading funded accounts have made this accessible to individual traders across FX, indices, and crypto markets. This article explains exactly how these models work, what they deliver, and how to position yourself to succeed within them.

Table of Contents

- What is no personal capital risk trading?

- Key benefits of trading without personal capital risk

- Comparing funded accounts to self-funded trading: pros and cons

- How disciplined risk management enables consistent performance without personal losses

- Common challenges and how to succeed in no personal capital risk funding

- Why no personal capital risk trading is a risk management upgrade, not just capital access

- Start your journey with DayProp’s funding programs

- Frequently asked questions

What is no personal capital risk trading?

No personal capital risk trading means you trade using capital provided by a proprietary trading firm, not your own money. Your personal savings are not exposed to market losses. Instead, you pay an evaluation or challenge fee to demonstrate your trading ability under defined conditions. Pass the evaluation, and the firm allocates funded capital for you to trade.

Proprietary trading firms allow access to financial markets without risking your own capital and enforce strict risk limits and profit sharing arrangements. The structure typically involves four core components:

- Evaluation fee: A one-time or recurring cost to enter a trading challenge, usually ranging from $50 to $800 depending on account size.

- Drawdown limits: A maximum allowable loss threshold, either daily or cumulative, that defines when an account is disqualified.

- Profit targets: A minimum return percentage required to pass the evaluation phase and receive funded status.

- Profit split: The percentage of trading profits you keep once funded, typically ranging from 70% to 90%.

Understanding what a funded trader is and how evaluation structures are designed helps clarify what you are signing up for. The key distinction is that your financial exposure ends at the evaluation fee. Once funded, trading losses reduce the firm’s capital allocation, not your bank account.

Key benefits of trading without personal capital risk

Trading without risking personal funds changes the calculus of every trade you place. The advantages extend beyond simply protecting your savings.

Access to capital you could not otherwise deploy. Most retail traders operating with personal funds manage accounts ranging from $1,000 to $10,000. Funded accounts commonly start at $25,000 and scale to $100,000 or more with increments tied to performance milestones. That buying power enables meaningful position sizing in major FX pairs, equity indices, and crypto markets.

Built-in risk controls prevent catastrophic losses. Scalable capital models separate skill from bankroll, rewarding traders who follow defined risk limits and maintain consistency over time. You are not permitted to blow an account in a single session. Daily loss caps and drawdown limits force a ceiling on downside exposure that many self-funded traders fail to impose on themselves.

Key benefits include:

- Personal capital safety: Your savings are not exposed to trade-level losses.

- Larger position sizing: Funded capital supports trades not possible on a small retail account.

- Profit sharing: You earn a majority of profits without putting up the capital base.

- Psychological discipline: Knowing only the challenge fee is at risk reduces panic-driven decision making.

- Scaling incentives: Consistent performance unlocks scalable funding benefits and higher capital allocations automatically.

“The advantages of low-risk investing through funded structures lie not just in capital access, but in the behavioral discipline the rules enforce.”

Pro Tip: When evaluating a funded account program, calculate the fee as a percentage of the target funded account size. A $200 fee for a $25,000 account is a 0.8% cost of entry. That context makes the risk-to-reward calculation clearer than treating the fee in isolation.

For a detailed breakdown of prop trading risk limits and how to work within them, structured reading helps before committing capital to any evaluation.

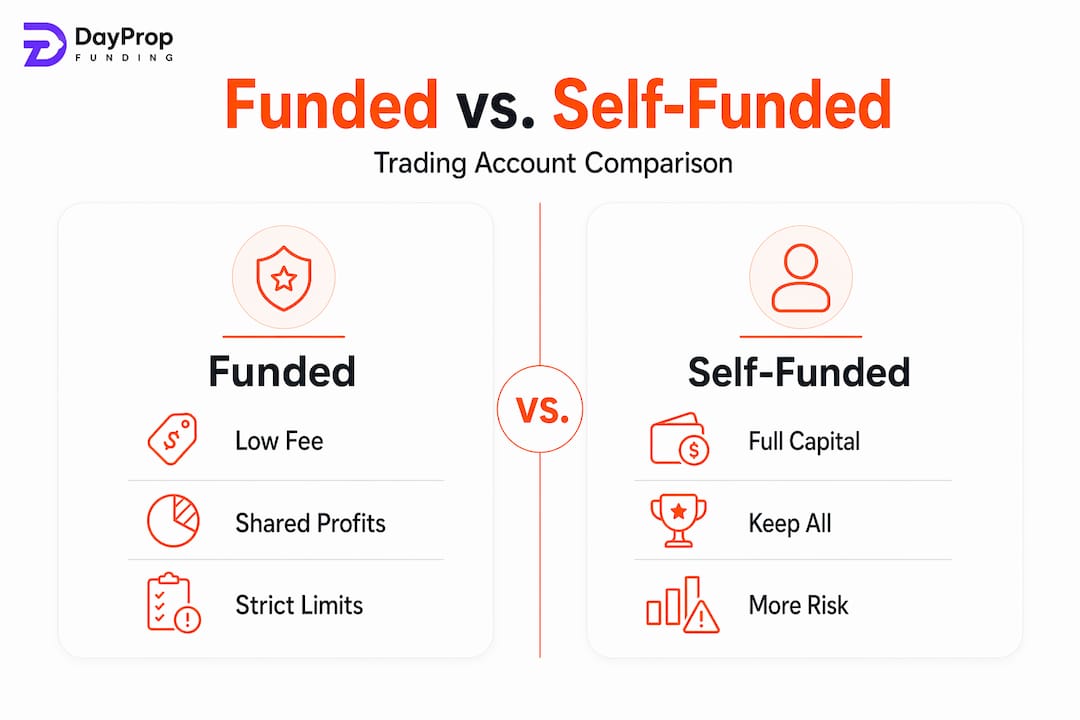

Comparing funded accounts to self-funded trading: pros and cons

Now that the benefits are clear, a direct comparison with traditional self-funded trading reveals the trade-offs involved.

| Factor | Funded account | Self-funded account |

|---|---|---|

| Capital required | Evaluation fee only | Full trading capital from personal savings |

| Tradable capital size | $25,000 to $200,000+ | Typically $1,000 to $20,000 |

| Profit share | 70% to 90% to trader | 100% to trader |

| Maximum personal risk | Evaluation fee | Entire account balance |

| Risk rules | Firm-imposed drawdown and daily limits | Self-imposed (often inconsistent) |

| Flexibility | Restricted by firm rules | Full discretion |

| Psychological pressure | Evaluation conditions and rule compliance | Direct financial loss anxiety |

| Earnings potential | Higher due to larger capital base | Limited by personal capital size |

| Ideal trader type | Disciplined, rule-based traders | Experienced traders with proven risk controls |

Prop firms offer no capital needed, with scaling possible, 70% to 90% of profits shared with the trader, and imposed discipline. The trade-off is reduced flexibility. Self-funded trading preserves full control but caps earning potential at the size of your personal account.

Tax treatment also differs by jurisdiction. Funded account profit shares are often treated as independent contractor income in many countries, whereas self-funded trading may qualify for capital gains treatment. Consulting a tax professional familiar with trading income is advised before committing to either model at scale.

To compare funding models across different structures before choosing, reviewing multiple programs side by side clarifies which evaluation conditions suit your trading style.

How disciplined risk management enables consistent performance without personal losses

The structural risk rules embedded in funded account programs do more than protect the firm’s capital. They build the kind of trading discipline that separates consistently profitable traders from those who blow accounts repeatedly.

The key rules most funded programs enforce:

- Daily maximum loss limit: Typically 4% to 5% of account value. Breach this and the account is closed. This rule alone prevents traders from revenge trading after a bad morning.

- Overall drawdown limit: Usually 8% to 10% of starting balance. This sets the outer boundary for how much the account can decline before the evaluation or funded status is revoked.

- Position sizing caps: Some programs limit maximum lot sizes or require stop losses on all trades. This prevents single-trade catastrophic losses.

These rules define loss limits and discourage revenge trading, enforcing consistency over time. The discipline is not optional. That is precisely why it works. And most prop firms enforce daily loss limits and maximum drawdown thresholds to keep traders solvent through market volatility.

Steps to adopt this risk mindset effectively:

- Set your personal daily maximum loss below the firm’s limit, giving yourself a buffer.

- Track rule adherence in a trading journal, not just profit and loss figures.

- Avoid increasing position sizes after wins. Scaling should follow account milestones, not emotional confidence.

- Review your worst trading days monthly to identify behavioral patterns.

Pro Tip: Build a drawdown playbook before you start trading any funded account. Write out exactly what actions you will take if you lose 2%, 3%, and 4% in a single day. Having predefined responses removes the decision-making pressure that leads to rule violations.

Detailed guidance on how to manage trading risk and build consistency is directly applicable to succeeding under funded account conditions. Reviewing forex risk management principles also reinforces the core mechanics of position sizing and stop placement.

Common challenges and how to succeed in no personal capital risk funding

Understanding risk discipline is vital, but operating within the prop firm environment presents specific practical challenges that require preparation.

Payout minimums and delays. Most funded traders require a $100 to $500 profit buffer and a minimum number of trading days before the first payout is processed. You may be profitable in week two and still need to wait until the end of the month.

Evaluation fees accumulate. Failing multiple evaluations is financially costly. A trader failing three $200 evaluations has spent $600 before earning a cent. This is a real cost that must be factored into income planning.

Income volatility is high. Serious prop trading often means running multiple accounts to diversify risk and ensure that one failed account does not eliminate all income for the month.

Practical steps to prepare:

- Save at least six months of living expenses before attempting to trade funded accounts full-time.

- Document three to six months of consistent profitability on a personal account before entering paid evaluations.

- Start part-time while maintaining another income source until funded account income is reliable and consistent.

- Track evaluation pass rates as a performance metric, not just trading profits.

Key actions to reduce income volatility:

- Run two to five active funded accounts simultaneously across different program providers.

- Keep evaluation fees as a monthly budget line, not an unexpected expense.

- Reinvest early profits into new evaluation fees rather than spending all payouts.

Pro Tip: Build a pipeline of challenges at staggered start dates so that you always have accounts in different phases of the funding cycle. When one account hits payout, another may be mid-evaluation, and a third may be newly funded. This reduces the income gaps caused by simultaneous account failures.

The trading evaluation guide outlines specific preparation steps, and understanding why passing prop challenges requires a different mindset than live trading helps avoid the most common failure patterns.

Why no personal capital risk trading is a risk management upgrade, not just capital access

Here is a perspective that most funded trading articles do not address directly: the primary value of no personal capital risk models is not the money. It is the behavioral structure they impose.

The biggest misconception is that access to more capital is primarily an income upgrade; it is actually a risk management upgrade. Traders who receive $100,000 in funded capital and proceed to trade it the same way they traded a $2,000 personal account almost always fail. Larger capital does not fix undisciplined execution. It accelerates the consequences of poor process.

The real shift that funded accounts force is cognitive. When you know that rule violations immediately terminate your funded status, you trade differently. You do not move stop losses. You do not add to losing positions. You do not take oversized trades to recover a bad day. These behaviors, which destroy self-funded accounts quietly over months, disqualify funded accounts immediately. The feedback loop is faster and more definitive.

This is why traders who focus on professional risk management practices before attempting funded evaluations outperform those who treat evaluations as lottery tickets. The process of qualifying for capital is itself a training system. Passing it consistently means your trading behavior is institutionally sound.

The financial security benefits that flow from this are compounding. A trader with repeatable, rule-compliant execution can scale capital indefinitely. A trader who chases profits without consistent risk processes will cycle through evaluation fees until they run out of capital or patience.

Pro Tip: Focus on perfecting rule adherence in the first 30 days of any funded account, not on maximizing returns. The scaling incentives built into most programs reward sustained consistency far more than a single profitable week.

Start your journey with DayProp’s funding programs

Now that you understand the advantages and challenges, here is how DayProp can help you access funded trading capital without risking your savings.

DayProp provides structured performance-based trading evaluation programs designed for disciplined retail traders in FX, indices, and crypto markets. The platform offers clear risk parameters, multiple scaling paths, and transparent rules so you know exactly what is required at every stage. Whether you are working through your first evaluation or managing multiple funded accounts, the trading evaluation guide covers the preparation steps in detail. Traders who have studied why evaluations fail and addressed those patterns consistently report stronger pass rates. DayProp’s programs are built around the same risk disciplines this article covers, rewarding process and consistency above all else.

Frequently asked questions

What does no personal capital risk mean in trading?

It means trading with funds provided by a firm instead of your own money, so your personal savings are not exposed to trade-level losses. Proprietary trading firms allow traders to use firm capital under strict rules without risking their own funds.

How do funded trading accounts protect my personal capital?

You only risk the evaluation or challenge fee, and trading losses are capped by firm-imposed drawdown and daily loss limits. Risk limits like drawdown caps keep traders solvent and protect personal finances throughout the trading process.

Can I make a living trading without risking my own capital?

Yes, but it requires consistent profitability, managing multiple funded accounts, covering evaluation fees, and maintaining a savings buffer. Making a living from prop trading often involves running 10 to 50 or more accounts with sufficient capital reserves.

What are the common drawbacks of no personal capital risk trading?

Drawbacks include evaluation fees, strict trading rules, payout minimums, reduced flexibility, and the pressure of challenge conditions. Prop firms impose strict rules and fees, and payouts require hitting minimum profit thresholds before any funds are released.

How can I prepare to succeed with no personal capital risk funded accounts?

Develop a proven trading edge on a small account, document consistent performance over several months, and master strict risk management before paying for any evaluation. Documenting consistent profitability before attempting challenges prevents wasted evaluation fees and improves long-term pass rates.

Recommended

- What is retail trading? A practical guide for new traders – DayProp Funding

- Why fund retail traders: benefits and challenges 2026 – DayProp Funding

- FX Trading Best Practices: Proven Strategies for Retail Success – DayProp Funding

- Master capital allocation in prop trading: retail guide – DayProp Funding