Many retail traders believe trading skill alone guarantees success in proprietary trading. Yet even profitable strategies fail without proper capital allocation. The difference between consistent funded traders and those who blow accounts often comes down to how capital is distributed across positions, time horizons, and market conditions. This guide clarifies capital allocation principles specifically for retail traders navigating FX, indices, and crypto prop challenges, providing evidence-based strategies to balance growth with survival.

Table of Contents

- Key takeaways

- Understanding capital allocation in proprietary trading

- Capital allocation models: fixed, dynamic, and hybrid approaches

- Risk-based sizing techniques and practical adjustments

- Balancing survival and growth: applying capital allocation for consistent prop trading success

- Enhance your prop trading with DayProp’s expert funding solutions

- FAQ

Key Takeaways

| Point | Details |

|---|---|

| Capital allocation basics | Prop firms allocate capital across traders, strategies, and asset classes to optimize risk adjusted returns while enforcing survival through drawdown limits. |

| Allocation models | Fixed allocation provides stability, dynamic allocation adapts to performance and volatility, and hybrids blend both approaches. |

| Risk based sizing | Risk based sizing uses rules like volatility targeting and the Kelly fraction to improve consistency and protect capital. |

| Market specifics | Forex markets have lower volatility, while crypto markets swing 24/7 demanding tailored allocation. |

Understanding capital allocation in proprietary trading

Capital allocation in prop trading means distributing firm-provided capital across traders, strategies, asset classes like FX, indices, and crypto, plus time horizons to optimize risk-adjusted returns while enforcing survival through drawdown limits and risk rules. Unlike personal trading where you control your entire account, prop firms impose strict parameters that determine how much capital you can risk per trade, per day, and across your portfolio.

This framework serves multiple purposes. First, it protects firm capital by preventing catastrophic losses from single positions or correlated bets. Second, it identifies traders who demonstrate genuine edge through consistent risk management rather than lucky streaks. Third, it creates scalable systems where successful traders receive more capital as they prove discipline.

Key components of prop trading capital allocation include:

- Maximum daily loss limits that trigger account restrictions

- Overall drawdown thresholds determining evaluation pass or fail

- Position sizing rules based on account equity percentages

- Correlation limits preventing overexposure to related instruments

- Time-based restrictions on holding periods and trading sessions

Market-specific allocation needs vary significantly. FX markets with lower volatility allow slightly higher position sizes, while crypto’s 24/7 price swings demand tighter controls. Indices fall somewhere between, with volatility clustering around economic releases and session opens. Understanding these distinctions helps you allocate capital appropriately across different prop challenges and funded accounts.

The difference between retail and institutional allocation models creates unique challenges. Retail traders must adapt institutional risk frameworks to smaller account sizes while maintaining the discipline that earns funding. This means thinking like a portfolio manager even when trading a single evaluation account.

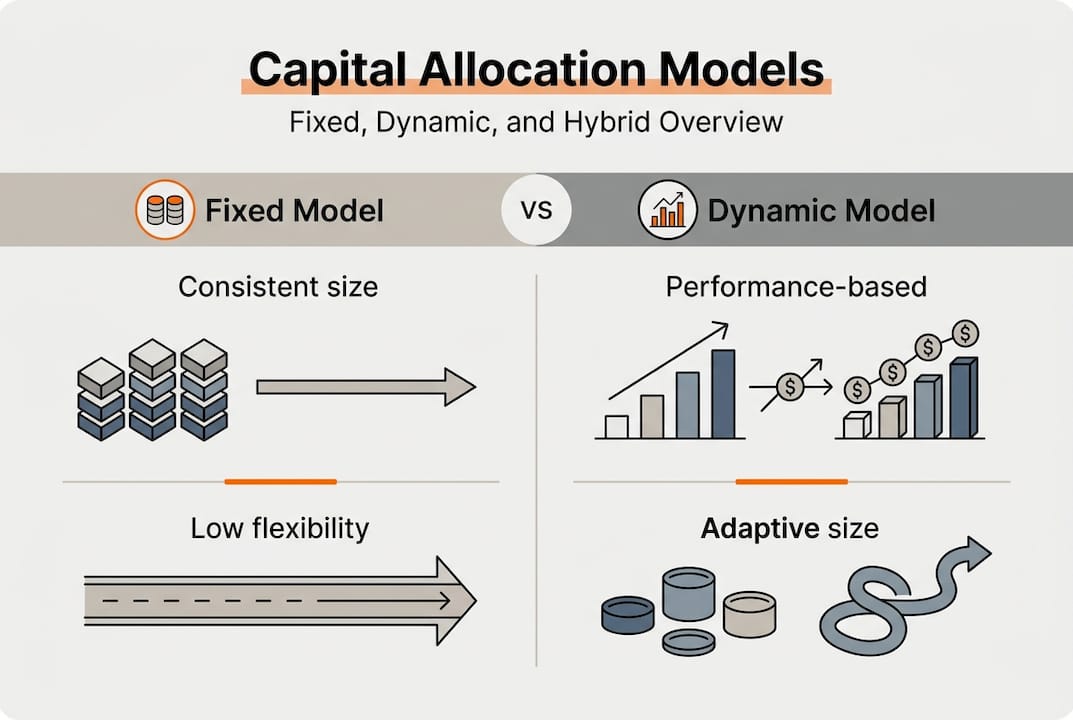

Capital allocation models: fixed, dynamic, and hybrid approaches

Prop traders employ three primary allocation models, each with distinct advantages for managing capital across market conditions. Fixed allocation maintains constant position sizes or risk percentages regardless of performance, providing stability and transparency. Dynamic allocation adjusts capital distribution based on rolling performance metrics, volatility signals, drawdown proximity, and market regime changes. Hybrid models combine both approaches to capture benefits while minimizing weaknesses.

| Model Type | Stability | Adaptability | Complexity | Best Use Case |

|---|---|---|---|---|

| Fixed | High | Low | Low | New traders building consistency |

| Dynamic | Low | High | High | Experienced traders with proven edge |

| Hybrid | Medium | Medium | Medium | Most retail prop traders |

Fixed models work well during evaluation phases when consistency matters more than maximizing returns. You risk the same percentage per trade regardless of winning or losing streaks, making performance easier to analyze and replicate. The main drawback is inflexibility when market conditions shift dramatically or when you approach drawdown limits.

Dynamic allocation adapts by increasing position sizes after profitable periods and reducing exposure during drawdowns or volatility spikes. This responsiveness helps capture opportunities when edge is strong while protecting capital when conditions deteriorate. However, dynamic models risk whipsaw effects where rapid adjustments amplify losses if signals prove unreliable.

Hybrid approaches dominate professional prop trading because they establish a fixed base allocation modified by performance and volatility signals. You might maintain 1% risk per trade as your baseline, then scale to 0.5% when daily loss reaches 2% or volatility exceeds historical norms. This combination prevents the rigidity of pure fixed models and the instability of pure dynamic systems.

Pro Tip: Avoid overreacting to short-term performance signals by requiring at least 20-30 trades before adjusting your allocation model. Single winning or losing days reveal nothing about edge, while premature changes often amplify emotional decision making that destroys prop accounts.

The choice between models depends on your experience level, market focus, and psychological tendencies. Newer traders benefit from fixed allocation’s simplicity and consistency requirements. Experienced traders with documented edge can leverage dynamic adjustments to optimize returns. Most retail prop traders succeed with hybrids that protect during drawdowns while allowing modest scaling during profitable periods.

Risk-based sizing techniques and practical adjustments

Risk-based position sizing methods translate capital allocation theory into specific trade execution rules that normalize risk across different instruments and market conditions. Volatility targeting, VaR budgets, and fractional Kelly criterion approaches help retail traders maintain consistent risk exposure regardless of whether they trade volatile crypto pairs or stable forex majors.

Volatility targeting adjusts position sizes so each trade contributes equal risk to your portfolio. If Bitcoin averages 4% daily moves while EUR/USD averages 0.6%, you would trade roughly 6.5 times more EUR/USD contracts to achieve equivalent risk. This normalization prevents volatile instruments from dominating your portfolio risk profile.

Value at Risk budgets allocate capital based on statistical loss probabilities over specific timeframes. A 95% daily VaR of $500 means you expect losses to exceed $500 only 5% of trading days. By budgeting total portfolio VaR, you can distribute capital across multiple positions while maintaining overall risk targets.

Fractional Kelly methods balance growth potential against ruin risk by using 0.25 to 0.5 times the full Kelly criterion recommendation. While full Kelly maximizes long-term growth mathematically, it produces stomach-churning drawdowns that violate prop firm limits. Fractional approaches sacrifice some growth for dramatically improved stability and survival probability.

Five practical considerations for retail traders managing capital allocation:

- Monitor liquidity and slippage costs that increase with position size, especially in crypto markets during off-peak hours

- Reduce allocation when edge appears to decay, such as strategy performance deteriorating over 50+ trades

- Incorporate macro signals like inflation spikes or central bank pivots that shift market regimes

- Apply tighter drawdown tolerance for crypto (3-5% daily max) versus forex (4-5%) due to 24/7 volatility exposure

- Deallocate capital from strategies that violate predefined rules, even during profitable periods

Capacity limits from liquidity constraints and slippage costs force allocation adjustments as account size grows. A strategy that works perfectly on a $10,000 evaluation may require complete redesign at $100,000 funded levels.

Pro Tip: Integrate macro-awareness into your allocation by reducing overall exposure 20-30% during extreme volatility regimes like central bank meeting weeks or major geopolitical events. This defensive positioning protects capital when correlations spike and typical diversification benefits disappear.

Crypto-specific allocation demands extra caution because markets never close. A 3% daily drawdown limit in crypto effectively provides less breathing room than 5% in forex that only trades 5 days weekly. Weekend gap risk in crypto also requires holding smaller positions Friday through Sunday or avoiding positions entirely during low-liquidity periods.

The key is matching your sizing technique to your trading style and market focus. Scalpers benefit from volatility targeting that normalizes tick-based risk. Swing traders prefer VaR budgets that account for multi-day holding periods. Position traders often use fractional Kelly to optimize growth over weeks and months while surviving inevitable drawdown periods.

Balancing survival and growth: applying capital allocation for consistent prop trading success

Successful prop trading requires allocating capital with survival as the non-negotiable first priority, then optimizing for growth within strict risk boundaries. This survival-first mentality separates funded traders who build long-term careers from those who experience brief success before inevitable account violations.

Empirical evidence demonstrates the power of optimized allocation. Research comparing allocation methods across 15 assets over 5 years found optimized Kelly portfolios delivered 22.86% annual returns with Sharpe ratio 1.15, while full Kelly approaches lost 21.44% and risk parity strategies lost 11.13%. The difference came entirely from how capital was distributed and rebalanced, not from superior market predictions.

| Strategy | Annual Return | Sharpe Ratio | Max Drawdown | Survival Rate |

|---|---|---|---|---|

| Optimized Kelly | 22.86% | 1.15 | 18.3% | 94% |

| Full Kelly | -21.44% | -0.34 | 67.8% | 31% |

| Risk Parity | -11.13% | 0.22 | 34.2% | 58% |

| Fixed 2% Risk | 14.52% | 0.89 | 22.1% | 87% |

Elite allocation strategies blend fixed base allocations with dynamic adjustments driven by performance signals and volatility measurements. Diversification across trading styles, time horizons, and asset classes reduces correlation risk. Macro-aware approaches that adjust risk based on economic regimes boost Sharpe ratios roughly 15% compared to static allocation methods.

Five actionable practices retail traders can implement immediately:

- Start every evaluation with fixed 1% risk per trade until you establish 30+ trade sample size proving edge

- Reduce position sizes by 50% when approaching 50% of maximum allowed drawdown

- Diversify across at least 3 uncorrelated instruments to prevent single-market disasters

- Track allocation performance weekly using Sharpe ratio and maximum drawdown metrics

- Implement hard stops on daily trading when losses reach 40% of daily limit

Pro Tip: Allocate capital across multiple time horizons by dedicating 60% to your primary strategy timeframe, 25% to longer-term positions that survive daily noise, and 15% to shorter-term tactical opportunities. This temporal diversification smooths equity curves and reduces psychological pressure from any single trade outcome.

Macro-aware adjustments enhance consistency by recognizing when market conditions favor your strategy versus when they create headwinds. During low-volatility grinding markets, mean-reversion strategies deserve higher allocation. When volatility expands and trends emerge, momentum approaches warrant increased capital. This dynamic rebalancing based on regime recognition prevents the common mistake of fighting market character with mismatched strategies.

The path to consistent prop trading success runs through disciplined capital allocation that prioritizes survival, diversifies risk intelligently, and adjusts dynamically to changing conditions. Traders who master these principles transform evaluation challenges into funded accounts and funded accounts into scaled capital that compounds over years. Those who ignore allocation eventually meet the statistical certainty of ruin, regardless of short-term wins.

Managing risk through proper allocation creates the foundation for consistent profits that prop firms reward with increased capital and payout opportunities. The difference between traders who receive funding once versus those who build sustainable careers lies not in prediction ability but in capital allocation discipline.

Enhance your prop trading with DayProp’s expert funding solutions

Mastering capital allocation theory means little without practical application in real prop trading environments. DayProp provides structured evaluation challenges designed specifically for retail traders ready to demonstrate professional-level risk management across FX, indices, and crypto markets.

Our performance-based evaluation process tests your ability to allocate capital effectively under realistic drawdown limits and profit targets. Detailed guides help you understand exactly what prop firms evaluate and how to optimize your allocation strategy for funding success. Whether you are attempting your first challenge or refining techniques after previous attempts, our comprehensive evaluation guide provides step-by-step frameworks for securing and maintaining funded status. Explore how DayProp bridges the gap between retail trading and institutional capital by funding disciplined traders who prove consistent edge through proper capital allocation.

FAQ

What is the main difference between fixed and dynamic capital allocation?

Fixed allocation maintains constant position sizes or risk percentages regardless of market conditions or recent performance, providing stability and predictability. Dynamic allocation adjusts capital distribution based on rolling performance metrics, volatility signals, and market regime changes to optimize returns. Hybrid models combine both approaches, using fixed base allocation modified by performance triggers to balance consistency with adaptability.

How can retail traders manage risk to avoid large drawdowns in prop trading?

Implement strict drawdown limits like 3% daily maximum loss and reduce position sizes by 50% when approaching half your total allowed drawdown. Apply risk-based position sizing methods such as fractional Kelly criterion or volatility targeting that normalize risk across different instruments. Maintain consistency by avoiding the temptation to increase risk after losses or chase short-term gains that violate your allocation plan.

Why is diversification important in capital allocation for prop trading?

Diversification spreads risk across multiple asset classes, trading strategies, and time horizons, reducing the impact of any single market event or failed trade on your overall account. Trading multiple instruments prevents correlation disasters where all positions move against you simultaneously. Proper diversification improves consistency metrics like Sharpe ratio that prop firms use to identify traders worthy of increased capital allocation.

How does volatility targeting improve position sizing in prop trading?

Volatility targeting adjusts position sizes so each trade contributes equal risk regardless of instrument volatility, preventing high-volatility assets like crypto from dominating your risk profile. By normalizing position sizes based on recent price movement, you maintain consistent risk exposure whether trading stable forex pairs or volatile indices. This approach improves portfolio stability and helps you stay within prop firm drawdown limits across different market conditions.

What makes fractional Kelly criterion better than full Kelly for prop traders?

Fractional Kelly methods using 0.25 to 0.5 times full Kelly recommendations dramatically reduce drawdown magnitude while sacrificing minimal long-term growth. Full Kelly maximizes mathematical growth but produces drawdowns exceeding 60% that violate all prop firm limits and destroy trader psychology. Fractional approaches balance growth potential with survival probability, making them practical for real-world prop trading where staying funded matters more than theoretical optimization.